Brexit has picked up momentum again, and so should the preparation for doing business after December 2020.

The aim of the ongoing Brexit negotiations is to reach an agreement that will govern the relationship between the UK and EU from 2021. For goods, as with all trade agreements that offer preferential duty rates (i.e. zero per cent or reduced as compared to the default, or ‘Most Favoured Nation (MFN)’, rate), this means there would be a set of preferential rules of origin to ensure the benefits do not leak to other unintended non-signatories to the agreement.

There is a common misconception that a trade agreement automatically removes any customs duty due. This is not the case. Businesses must evidence that the rules of origin are met if they want to benefit from the trade agreement, and this can be a complex process.

This article explains the preferential rules of origin, and why the food and drink industry should care about them, both in the context of Brexit and beyond. It also outlines a few practical action points for businesses to take now.

What are rules of origin?

The European Commission defines origin as the ‘economic nationality’ of goods traded in commerce[1]. Preferential rules of origin dictate how origin is determined in the context of trade agreements. There are two categories of rules of origin:

- Wholly obtained. For example, if a product is grown in country A, or if the product is processed from what is grown in country A without incorporating materials of any other country.

- Sufficiently transformed. There are three different types of rules to determine when a product has been sufficiently transformed. Depending on the product, one or more of these rules could be applicable:

- the ‘value added’ rule which limits the non-originating material used to make the final product;

- the change of tariff classification rule which requires the final product to be manufactured from materials of any tariff heading except that of the final product; or

- there may be specific non-originating materials permissible in the manufacture of the final product.

If the UK and the EU are to reach a trade agreement by the end of 2020, there would need to be a set of rules of origin for each of the products covered by the trade agreement.

If agreement between the UK and the EU is reached, what will the rules of origin be?

While it is unclear what rules will be adopted, the existing rules of origin in recent EU trade agreements offer good indications. The UK’s approach to negotiations[2], as published in February 2020, made references to rules of origin in the EU-Japan Economic Partnership Agreement (EPA) and the EU-Canada Comprehensive Economic and Trade Agreement (CETA). The provisions of rules of origin are based on the Harmonised system of classification.

Here are some examples taken from these two agreements. The same food (i.e. Chapter 4 of the Harmonised System) and drink (i.e. Chapter 22 of the Harmonised System) items are listed below for comparison.

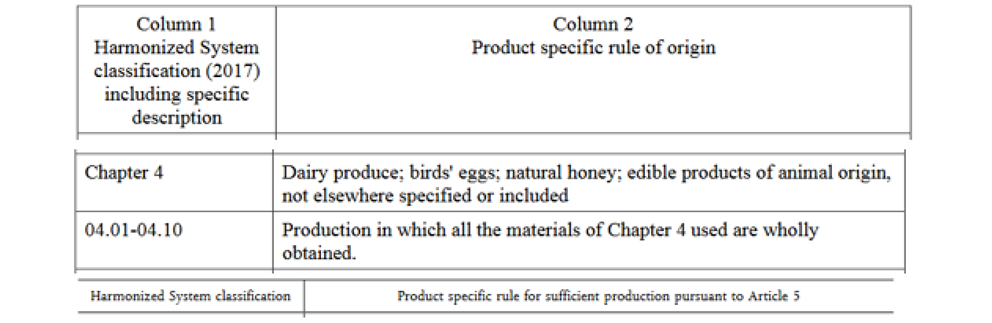

Example 1: EU-Japan EPA: Annex 3-B[3], product specific rules of origin for chapter 4

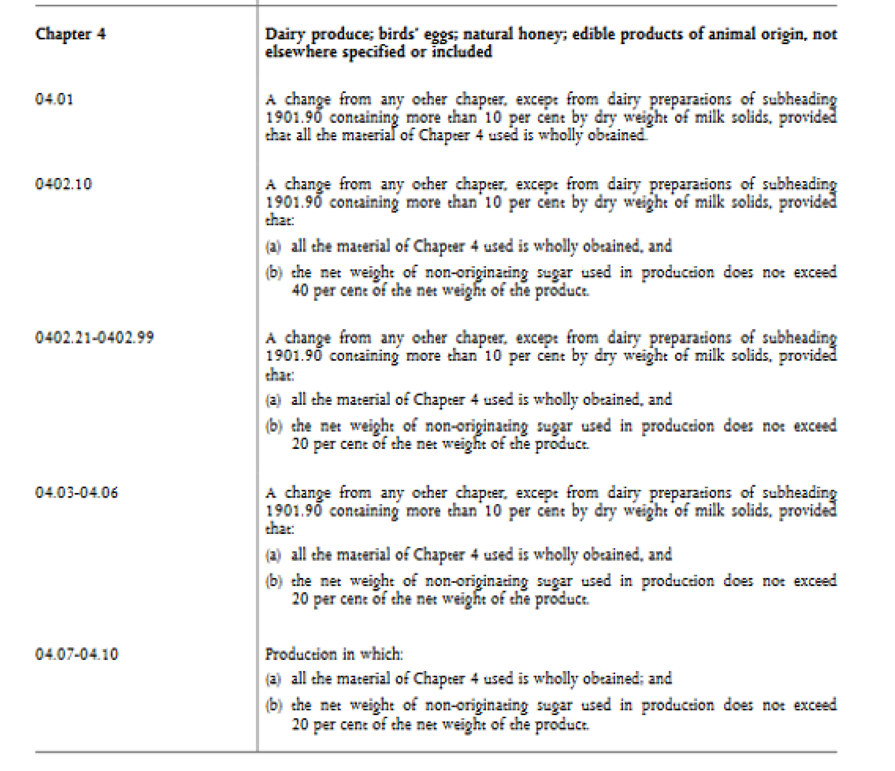

Example 2: EU-Canada CETA: Annex 5[1], product specific rules of origin for chapter 4

![]()

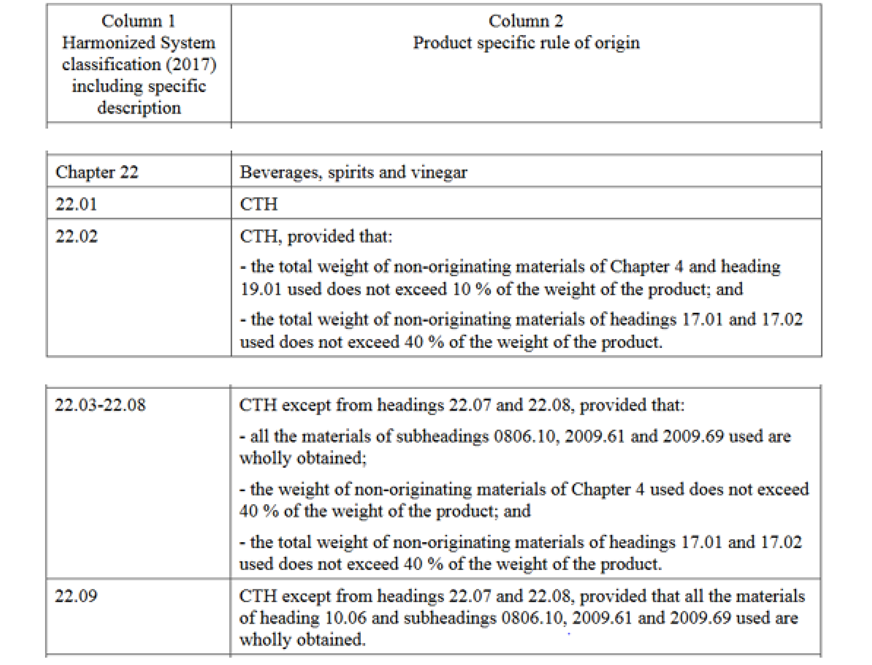

Example 3: EU-Japan EPA: Annex 3-B, product specific rules of origin for chapter 22

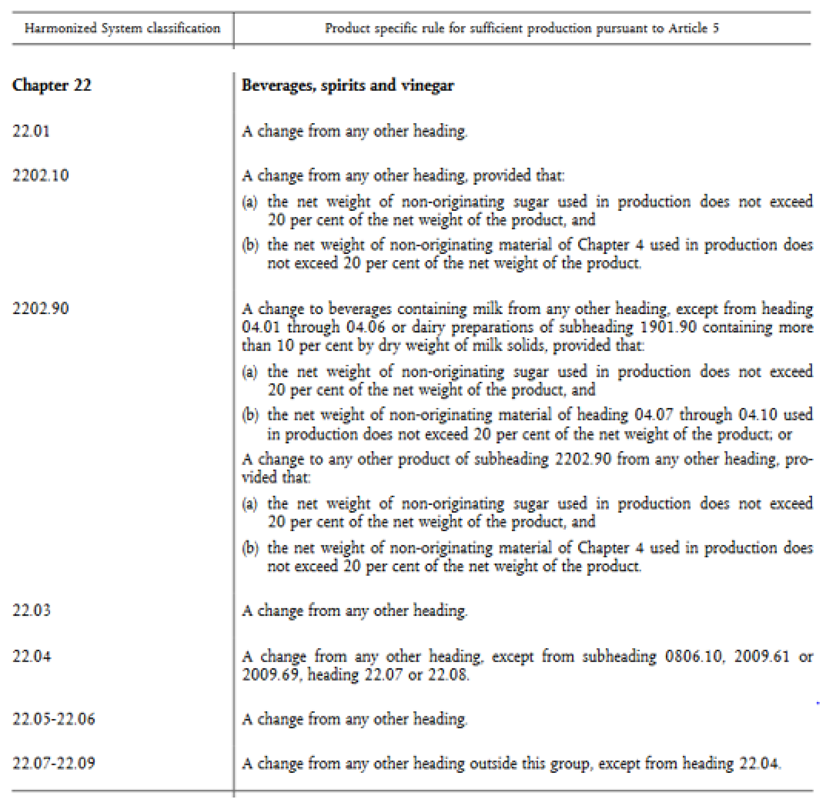

Example 4: EU-Canada CETA: Annex 5, product specific rules of origin for chapter 22

Why should food and drink businesses care about rules of origin?

The examples taken from the EU-Japan EPA and the EU-Canada CETA show different trade agreements can have different rules of origin for the same product. Grappling with, and understanding, the key issues around rules of origin now will help food and drink businesses get ahead of the game on planning for the future. Particular issues to consider are:

1. Rules of origin are complex and there are uncertainties

As illustrated in the examples taken from the EU-Japan EPA and EU-Canada CETA, the rules of origin for the same goods (e.g. dairy produce) vary in complexity and specifications in existing agreements. Given that businesses have different operations and source raw materials differently, it would be useful to understand whether, and how, they would meet the differing sets of rules. The challenge is to identify exactly what a business’s current processing operations are, and then apply the rules of origin to check whether the finished goods would meet existing rules as things stand. If not, consider what can be done (both internally and externally) to meet them. The financial impact of meeting rules of origin which attract zero per cent customs duty can be significant compared to the alternative of attracting high duty rates (e.g. the EU applies 17.3 per cent customs duty on natural honey[1]).

2. Classification is key, but allocating a commodity code that determines which rules of origin apply can be challenging

Currently, there is no need to file a customs declaration when goods move between the UK and the EU. This means that unless a business is submitting Intrastat declarations (i.e. businesses which in the last calendar year, moved more than £250,000 worth of goods to countries in the EU or received more than £1.5 million worth of goods from countries in the EU), it is unlikely that those goods have had a commodity code allocated to them. Even where commodity codes have been allocated to products due to Intrastat declaration requirements, they should be used with caution. Intrastat declarations are made for statistical purposes, so businesses often spend insufficient time on checking the accuracy of the commodity codes allocated.

The process of allocating commodity codes can be tricky for food and drink products, as many pieces of information are required to make the correct decision. If the wrong commodity code is used, a business may be looking at the wrong rules of origin, as they are organised by commodity code. Therefore, it is crucial to get the classification right.

Note that even if there is no trade agreement between the UK and the EU, commodity codes are still required as they determine which customs duty rates are applicable.

3. Not meeting the rules of origin, or the inability to evidence them, can lead to additional costs

Food and drink products tend to attract high ad valorem customs duty rates as well as specific duty rates. For businesses selling to the EU-27 Member States post Brexit, customs duty due on their products would make them less competitive.

Even if there is a trade agreement between the UK and the EU, it does not automatically remove the customs duty due. This is because the origin status needs to be evidenced. In existing EU trade agreements, origin is evidenced through a declaration or origin certificates. Businesses may wish to consider reviewing existing contracts with suppliers and customers to address challenges relating to meeting rules of origin.

Businesses buying from the EU-27 Member States post Brexit would also face additional costs if the goods do not meet the rules of origin of a UK-EU trade agreement, or if origin is not evidenced. This is because the goods would then be treated as imports from a third country. Goods imported from a third country attract customs duty rates listed in the UK Global Tariff (UKGT), the UK’s new MFN tariff regime applicable from 1 January 2021. Most food and drink products (e.g. dairy produce) are subject to high customs duty rates or specific duty rates under the UKGT.

What can businesses do now to prepare?

There are actions food and drink businesses can take now, to be informed and be in a position to actively shape future UK trade agreements.

It is important to note that these efforts would not be wasted if the UK and the EU do not end up agreeing on a trade agreement, as the activities below would still help businesses to prepare for the alternative scenario (e.g. trading under World Trade Organisation rules). They would also be helpful should businesses wish to express their concerns or demands for future trade agreements between the UK and a third country other than the EU.

Top five action points:

- Increase visibility over your current operations. Gather information such as the exact processing activities, and identify any blind spots

- Allocate commodity codes to each of the relevant products that will be crossing the UK-EU border

- Review your operations against the possible sets of rules of origin for the relevant commodity codes in order to check their eligibility

- Formulate your concerns / requests, back them up with evidence and analysis so that they can be communicated to the relevant stakeholders

- Review existing contracts with suppliers and customers to anticipate any challenges you may face relating to meeting rules of origin.

For further guidance and help with the actions listed above, please get in touch with our Food and Drink team or Jessica.

[1] https://trade.ec.europa.eu/tradehelp/basic-rules

[2]https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/868874/The_Future_Relationship_with_the_EU.pdf

[3] http://trade.ec.europa.eu/doclib/docs/2018/august/tradoc_157231.pdf#page=65

[4] https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:22017A0114(01)&from=EN

[5] http://publications.europa.eu/resource/cellar/4fdaf64e-fc25-11e9-8c1f-01aa75ed71a1.0006.01/DOC_1