The UK’s new rules for international individuals and their structures: a high level summary

25 Jun 2025

7 min read

This website will offer limited functionality in this browser. We only support the recent versions of major browsers like Chrome, Firefox, Safari, and Edge.

The UK’s non-dom regime was replaced from 6 April 2025, and the new legislation made various changes relevant to individuals and structures with an international connection.

The UK’s “non-dom regime” was replaced on 6 April 2025.

The new rules focus on a person’s tax residency rather than domicile and are potentially relevant to:

This is a high level summary of the new rules and their impact. More detail can be found here.

Please note that double tax treaties can change the impact of the new rules in practice and so also need to be considered.

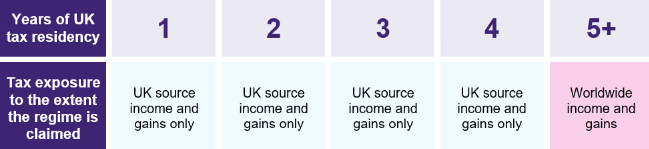

The new 4-year FIG regime

Individuals who are tax resident in the UK are generally subject to UK tax on their worldwide income (at a rate of up to 45%) and worldwide gains (at a rate of up to 24%).

However, the new regime can completely exempt most forms of foreign income and gains from these UK taxes during a person’s first four years of UK tax residency. Such “FIG” can also be used in the UK without a tax charge:

Any individual can access the 4-year FIG regime as long as they have been non-UK tax resident for at least 10 consecutive tax years before the first of the four years (UK tax years run from 6 April one year to 5 April the next).

It does not apply automatically and individuals can choose which of the four years to claim it in (if any). All foreign income and gains must be reported in the UK whether the relief is claimed or not.

Whilst there is no charge for using the 4-year FIG regime, it does have some drawbacks. For example, in the years for which they claim it the individual will lose some tax allowances and the ability to deduct foreign losses from taxable gains.

The 4-year FIG regime can also apply to employment income derived from duties performed outside of the UK although it is subject to a cap in these circumstances.

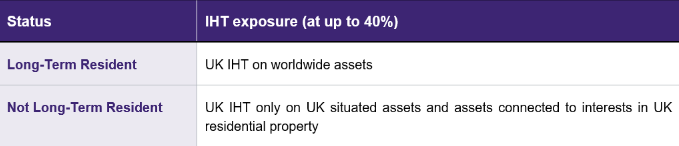

The new rules for inheritance tax

The extent of an individual’s exposure to UK inheritance tax (“IHT”) now depends largely on whether they are a “Long-Term Resident”:

A person will generally become “Long-Term Resident” in a given tax year if they have been tax resident in the UK for at least 10 of the preceding 20 tax years.

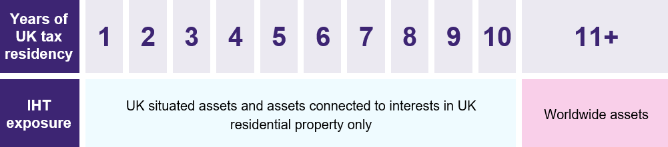

The simplest example of this would be someone who moves to the UK and becomes Long-Term Resident at the beginning of their 11th consecutive year of UK tax residence:

Once someone becomes Long-Term Resident, they retain that status:

Changes for previous remittance basis users

Although the remittance basis has been replaced going forwards, it will remain highly relevant to many who used it in the past.

In particular, foreign income and gains which benefited from the remittance basis in previous tax years can still trigger a taxable remittance after 6 April 2025. Indeed, the scope of what amounts to a remittance has actually been broadened.

Existing segregated account structures may therefore need to be retained.

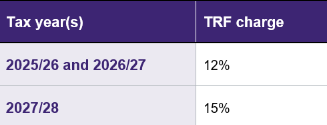

However, there is now a “Temporary Repatriation Facility” (the “TRF”) which can be used to turn historic foreign income and gains into “clean capital” (i.e. into funds which can be used in the UK without a tax charge).

This is a temporary measure available until 5 April 2028 and can be accessed by paying the TRF charge of either 12% or 15% on the amount being converted into clean capital:

Either charge represents a very significant discount as compared to the usual tax rates of up to 45%.

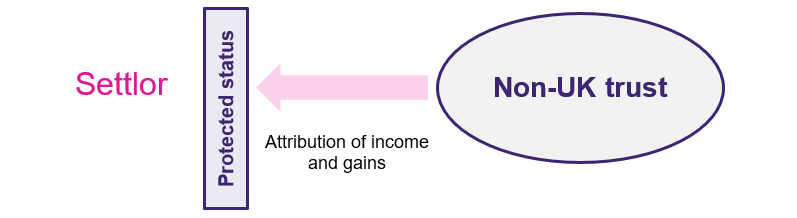

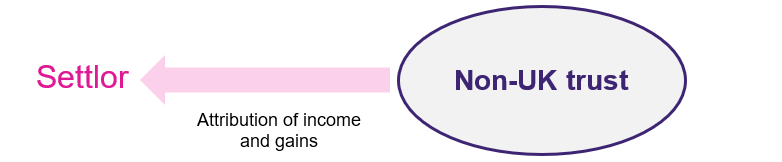

Loss of protected status – increased risk of tax for the settlor

Until 6 April 2025, many non-UK resident trusts settled by non-UK domiciled individuals benefited from “protected status” such that income and gains realised within the structure were (with some notable exceptions) blocked from being taxed on the settlor:

From 6 April 2025, protected status has been stripped away from these trusts, such that the circumstances in which income and gains will be attributed to, and taxed on, UK resident settlors have been broadened significantly:

This is primarily an issue for non-UK resident trusts with living, UK tax resident settlors. Various factors, including the beneficial class of the trust, the investment profile and whether the settlor can claim the 4-year FIG regime, will determine the actual extent of a settlor’s UK tax exposure as a result of this change.

Changes to the taxation of beneficiaries

Whilst the tax regime for beneficiaries is largely unchanged, they may now be able to claim the 4-year FIG regime in relation to what they receive from trusts.

Separately, beneficiaries who have been subject to the remittance basis in the past may be able to claim a version of the TRF to pay 12% or 15% on certain forms of distribution or benefit received between now and 5 April 2028 (rather than the usual rates of up to 45%).

If the funds or assets being distributed are within the scope of UK IHT (see below) there could also be IHT charges on a distribution regardless of where the beneficiary is resident.

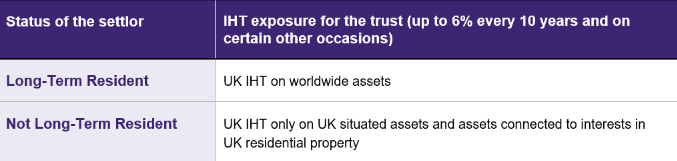

Inheritance tax for trusts

The inheritance tax status of trusts whose settlors died before 6 April 2025 is generally unchanged.

For discretionary trusts with living settlors, their status will now usually be dependent on whether the settlor is Long-Term Resident:

For some settlors this change could also increase the IHT exposure on their death.

If the settlor loses Long-Term Resident status then this can trigger an “exit charge” of up to 6% on the value of non-UK situated assets in the trust at that time.

Exit charges can also be triggered by distributions of funds or assets which are within the scope of IHT.

Whilst tax residence has broadly replaced domicile as the key factor determining exposure to UK tax, an individual’s domicile status can still have a material impact on them.

Just by way of example, domicile can be relevant to the application of certain double tax treaties and can determine which country’s laws apply to succession to a person’s estate.

We have a vast amount of experience advising individuals with international connections and their structures.

We can advise you as to how the new regime might impact you, help you plan your affairs accordingly and assist you in making the most of the transitional rules.

![]() Legal updates

Legal updates

4 August 2026

![]() Thought leadership

Thought leadership

29 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-29-15-31-18-835-6a6a1cc67b233ab23d62a576.jpg)

![]() Thought leadership

Thought leadership

27 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-14-17-26-18-947-6a56713a0b21ee7f9d8cc22f.jpg)

![]() Thought leadership

Thought leadership

20 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-20-16-45-25-984-6a5e50a53778c07e459eb63a.jpg)

![]() Thought leadership

Thought leadership

2 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-01-14-49-03-555-6a4528df2871f60bca6453f5.jpg)

Want more Burges Salmon content? Add us as a preferred source on Google to your favourites list for content and news you can trust.

Update your preferred sourcesBe sure to follow us on LinkedIn and stay up to date with all the latest from Burges Salmon.

Follow us