Family Investment Companies (FICs): What you need to know

18 May 2026

6 min read

This website will offer limited functionality in this browser. We only support the recent versions of major browsers like Chrome, Firefox, Safari, and Edge.

This guide explains how Family Investment Companies (FICs) are used in practice, why they are popular in UK tax and succession planning, and where they can add real value. We explore different FIC structures, their tax treatment, and the key considerations for families deciding whether this approach is right for them.

A “Family Investment Company” or “FIC” is a term used to refer to a company which holds family investment assets (generally not trading assets), such as investment properties or a portfolio of quoted shares and bonds.

FICs can be an attractive option for succession planning and general UK tax planning because they:

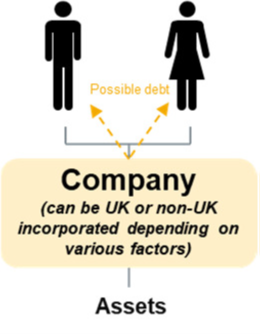

Some FICs are intended primarily to reduce ongoing exposure to UK tax on investment returns.

Such a FIC might be wholly owned by the individual or couple who generated the wealth:

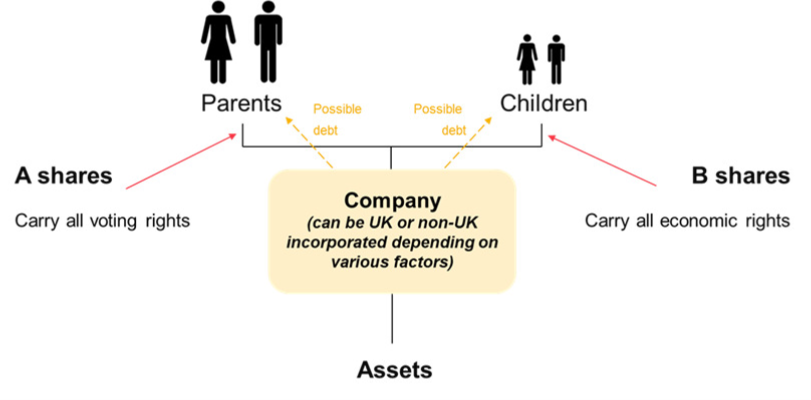

Other FICs are intended primarily to act as an estate planning tool by allowing one generation to pass the value of assets to a younger generation without also handing over control.

This type of FIC generally has at least two classes of share – “A” shares which have voting rights and “B” shares which carry economic rights.

Typically the individuals funding the company (usually the parents) are appointed as initial directors and retain the A shares. They therefore have control over the FIC and its assets (including making investment decisions) and determine matters such as whether a dividend is declared.

The B “economic shares” are generally passed on to the next generation.

Most of the value of the FIC is in the B shares and, provided the parents survive for seven years after gifting these to their children, those shares should be outside of the scope of UK inheritance tax on the parents’ deaths.

A simple example of this type of FIC structure would be:

One of the advantages of a FIC is that it can be tailored to a particular individual’s or family’s situation and needs. For example, there are much more complicated versions of the planning which include many different share classes to allow for more tailored treatment of the economic rights.

The taxation of FICs is often a key driver for considering them. They can offer a lower tax environment than, say, personal ownership and trusts, particularly on the accumulation of income, and this can allow wealth to grow more quickly. For example:

However, tax will always need to be considered carefully as there are some downsides. For instance, the 25% corporation tax rate is marginally higher than the 24% rate which individuals generally pay on gains and some tax reliefs available to individuals are not available to FICs.

Furthermore, if profits are subject to 25% tax within a FIC and are then distributed to shareholders who pay income tax on their dividend, the total effective tax rate can be closer to 54.5%.

As a result, FICs tend to be most tax efficient when their investments are tailored to take advantage of their particular tax treatment, and if returns are reinvested over the medium or long term.

As a general rule of thumb we would suggest that FIC planning becomes viable once the intention is for the FIC to hold at least £2m of investments.

Above this threshold FICs can scale very well and be used to hold much larger portfolios if required.

The exact circumstances in each case will determine how best to set up the FIC.

Relevant questions include:

There are a number of ways to fund a FIC (including by subscription for shares or loan funding), each of which has advantages and disadvantages.

Choosing the right method for a particular individual or family’s circumstances is a key part of good FIC planning.

Thought should be given as to whether the FIC should be incorporated in the UK or elsewhere.

If in the UK, the company can be limited or unlimited. Limited companies offer limited liability for their shareholders whereas unlimited companies do not. However, unlimited companies offer more flexibility in some instances and do not have to file accounts (providing certain conditions are met), so offer slightly more privacy.

Explore our full private wealth offering and expertise using the link below.

Learn more

![]() Thought leadership

Thought leadership

2 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-01-14-49-03-555-6a4528df2871f60bca6453f5.jpg)

![]() Legal updates

Legal updates

1 July 2026

![]() Legal updates

Legal updates

9 June 2026

![]() Legal updates

Legal updates

2 June 2026 • 8 min read

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-05-12-11-03-07-025-6a0308ebab2914b0981e857f.jpg)

![]() Legal updates

Legal updates

28 May 2026 • 8 min read

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-05-22-14-59-49-166-6a106f655c3b7f033260eac7.jpg)

Want more Burges Salmon content? Add us as a preferred source on Google to your favourites list for content and news you can trust.

Update your preferred sourcesBe sure to follow us on LinkedIn and stay up to date with all the latest from Burges Salmon.

Follow us