Pensions and IHT after 6 April 2027: Key points for private client advisers

1 Jul 2026

12 min read

This website will offer limited functionality in this browser. We only support the recent versions of major browsers like Chrome, Firefox, Safari, and Edge.

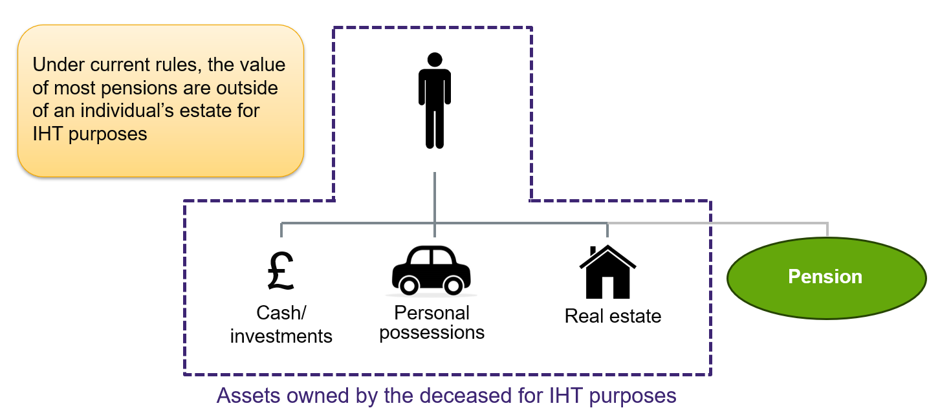

From 6 April 2027, the inheritance tax (IHT) treatment of pensions will change fundamentally. Most unused pension funds and pension death benefits will be brought within the value of a deceased person’s estate for IHT purposes, ending the long‑standing position under which pensions often sat outside the IHT net.

This article focuses on the technical framework underpinning the reforms, considers the latest HMRC technical note (updated 29 May 2026), and highlights points private client practitioners should be aware of in practice.

This article is part of a series on the changes to IHT on pensions:

The reforms were announced at the Autumn Budget with the purported goal of realigning pensions with their primary purpose (i.e. funding retirement), rather than being used as IHT efficient vehicles for passing assets to the next generation.

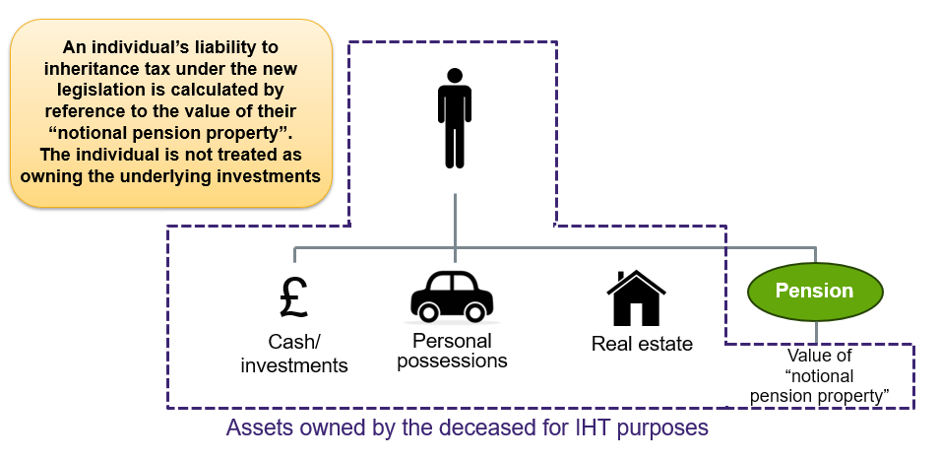

The new legislation, implemented under the Finance Act 2026 1, creates a new deemed asset, “notional pension property”, which has the value of an individual’s unused pension entitlements at death. This notional pension property is then aggregated with the rest of that individual’s estate for the purposes of calculating IHT on their estate. This is a change from previous versions of the legislation, which deemed the underlying pension assets to be part of the estate. As is explained in more detail below, this change is particularly relevant for those who are not Long-Term UK Resident for IHT purposes. A comparison of the current position against the new approach is illustrated below.

Subject to exemptions, notional pension property will generally include:

from registered pension schemes, qualifying non-UK pension schemes and section 615(3) schemes.

However, there will be various reliefs and some entitlements remain out of scope of IHT as follows:

Business property relief (BPR) and agricultural property relief (APR) do not apply to notional pension property, because the pension holder is not treated as owning the underlying assets.

There is also no loss-relief on the notional pension property (i.e. IHT is payable on the value of such property at the date of death, even if the value has fallen by the time investments are liquidated).

The changes should also be considered against the backdrop of the UK’s new residency-based test to determine IHT exposure, introduced from 6 April 2025.

In brief:

For LTR individuals, IHT will apply to the value of their notional pension property regardless of where the pension scheme is based.

For non-LTR individuals, IHT will apply only to notional pension property from schemes established in the UK. QNUPS and QROPS (i.e. non-UK established schemes) should therefore be outside of the scope of the charge for non-LTRs.

Because the pension value is by reference to a value of ‘notional property’ and not the underlying assets, there is no need to identify the situs of each underlying investment within a deceased’s pension plan. It is the status of the pension plan itself which determines whether the notional pension property is considered UK situated for these purposes.

The fact that “notional pension property” (i.e. a fictional asset, the value of which is determined by relevant pension entitlements) is treated as part of the estate, as opposed to underlying pension assets, has a number of practical implications:

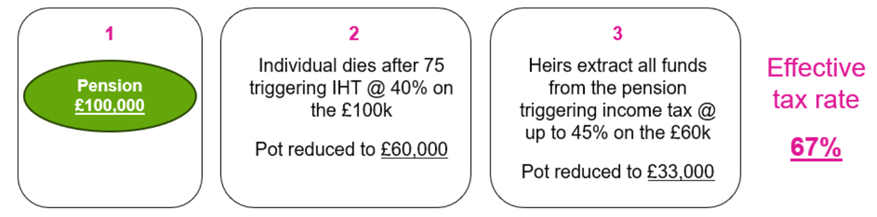

Where a pension holder dies aged 75 or over, pension death benefits are potentially subject to both IHT and income tax. Where IHT has been paid on a beneficiary’s share of notional pension property, the amount subsequently subject to income tax is reduced proportionately. A form of credit applies to achieve the same overall result if the IHT is paid from another source and not directly from the pension pot.

This is intended to prevent straightforward double taxation. However, it does not eliminate high effective tax rates, as illustrated below:

The effective rate can climb even higher, up to 89% (or 91% in Scotland) if the addition of the pension into the deceased’s taxable estate causes them to lose access to the Residence Nil Rate Band.

One significant (and potentially under‑appreciated) consequence of bringing pensions into charge is the impact on the Residence Nil Rate Band (RNRB).

RNRB is currently available where a qualifying residence passes to direct descendants, but it is tapered away once the value of the estate exceeds £2 million, reducing by £1 for every £2 over that threshold.

From April 2027, the value of notional pension property is included when testing whether the £2 million threshold is exceeded. This means that estates which previously fell comfortably below £2 million may now be pushed above the taper point because of their pension value, which can be a significant asset for individuals.

In practice, this can produce a double impact:

Combined with income tax mentioned above, this can result in extremely high effective tax rates!

The new regime will require practical information-sharing between personal representatives (PRs), pension scheme administrators (PSAs) and beneficiaries. In practice, PRs will need to identify relevant pension arrangements early, notify the PSA of the death and request information about the value and nature of the pension death benefits. The PSA will then need to provide the information needed for the PRs to calculate and report the IHT position, including where pension death benefits are to be paid outside the estate.

Withholding notices are expected to be an important protection for PRs. Broadly, once PRs have enough information to identify a potential IHT liability attributable to pension property, they should be able to require the PSA to withhold up to 50% from the in scope pension death benefits for a period of time (not exceeding 15 months from the person’s death). This should help prevent the scheme from paying the full amount to beneficiaries before the IHT position has been finalised, reducing the risk that PRs have to recover tax from beneficiaries after the event.

Payment notices can provide a mechanism for pension-related IHT to be paid from the pension scheme itself. Once the IHT position has been calculated, PRs can issue a payment notice requiring the PSA to pay the relevant amount to HMRC from the withheld pension funds directly. This will be particularly important where the estate itself is somewhat illiquid, or where the pension represents a large proportion of the overall taxable estate.

HMRC’s technical note states that a prospective PR cannot issue a payment notice. Under the legislation, a prospective PR is “a person who has reason to believe that they will become a personal representative” of the deceased.

This leaves a practical question as to whether an executor named in a Will, who derives authority from the Will rather than the grant, may issue a payment notice before probate is obtained, as distinct from an administrator on intestacy who derives authority from the grant of letters of administration. There is a respectable argument that named executors should be able to do so, but the point would benefit from confirmation in HMRC guidance.

It is also worth noting that the general definition of “personal representative” in the Inheritance Tax Act 1984 can include a person who has assumed responsibility for administering the estate. If correct, that may give any such person sufficient standing to issue a payment notice under the new rules, even before the grant of representation is obtained. This would be a more practical interpretation: PRs routinely authorise direct payments of IHT to HMRC from other institutions before the grant, and it would be difficult to justify a materially different approach for pension schemes. The point is not yet free from doubt, and further guidance will hopefully clarify the position.

Further regulations and guidance are expected in the coming months. While we do not anticipate any material changes to the substance, the additional detail should help clarify how the changes are expected to operate in practice.

Advisers should be encouraging clients to review their pension nominations, ensure appropriate executors are named in Wills, and consider their possible IHT exposure (including any impact on RNRB), as well as their estate liquidity, well in advance of 6 April 2027.

This article reflects the position based on HMRC’s technical note as at 29 May 2026.

1 Sections 66 to 71 of the Finance Act 2026, which received Royal Assent on 18 March 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-01-12-30-27-638-6a45086355254589a9194c78.jpg)

![]() Legal updates

Legal updates

1 July 2026

![]() Thought leadership

Thought leadership

30 June 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-06-30-09-43-00-281-6a438fa4a83b787e5f246eab.jpg)

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-06-29-09-14-29-111-6a42377570265166a19fc034.jpg)

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-06-26-17-57-39-585-6a3ebd93cd48266713b183af.jpg)

![]() Thought leadership

Thought leadership

25 June 2026

/Passle/5d9604688cb6230bac62c2d0/MediaLibrary/Images/6051d455535488026031c917/2021-03-30-22-00-49-559-60639f9153548906000ad9ab.JPG)

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-06-17-10-48-04-068-6a327b647c4c17890fc51f0e.jpg)

/Passle/5d9604688cb6230bac62c2d0/MediaLibrary/Images/5f37f1285354880c64118596/2023-02-21-13-23-45-555-63f4c5e1f636e9107857282f.jpg)

![]() Thought leadership

Thought leadership

22 June 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-06-22-13-14-36-100-6a39353c5e574b7f907bf2c1.jpg)

Want more Burges Salmon content? Add us as a preferred source on Google to your favourites list for content and news you can trust.

Update your preferred sourcesBe sure to follow us on LinkedIn and stay up to date with all the latest from Burges Salmon.

Follow us