Family Investment Partnerships (FIPs): What you need to know

19 Jun 2026

7 min read

This website will offer limited functionality in this browser. We only support the recent versions of major browsers like Chrome, Firefox, Safari, and Edge.

This guide explains how Family Investment Partnerships (FIPs) are used in practice, why they are popular in UK tax and succession planning, and where they can add real value. We explore different FIP structures, their regulatory and tax treatment, and ongoing operation.

“Family Investment Partnership” or “FIP” is a term used to refer to a partnership arrangement which holds family investment assets.

FIPs can allow the value of such assets to be passed on to the next generation in a controlled manner, reducing the value of the older generation’s estates for tax purposes whilst placing restrictions on the access the next generation has to the wealth.

The younger generation are often children or grandchildren but this note refers to children for simplicity.

Whilst FIPs are less well known than Family Investment Companies or trusts, they can be very effective when used correctly.

They have particular value when the alternatives are unattractive, such as in the context of UK/US planning where:

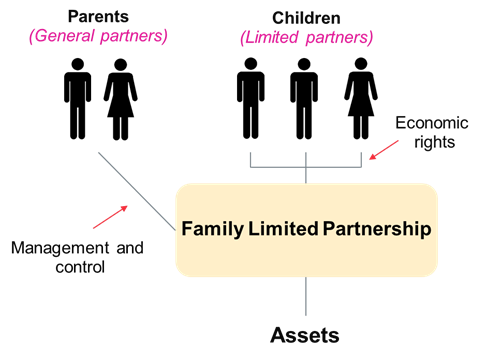

FIPs can take a number of different forms but a popular option is a “limited partnership” because this allows the older generation to retain greater control over the wealth being transferred.

A limited partnership creates two distinct types of partnership interest:

The general partner interests are usually held by the generation establishing the FIP whilst the limited partner interests are given to the next generation.

Such a FIP might look like this:

In practice the general partnership interest is sometimes held via a corporate (for limited liability) and it can be helpful from a US perspective for one parent to fund the FIP whilst the other holds the general partnership interest (whether directly or indirectly).

There have previously been concerns as to whether FIPs could fall within the UK’s regulatory regime for collective investment schemes. However, the UK regulator (the Financial Conduct Authority) has issued favourable guidance for family investment vehicles which invest only private wealth.

A key reason to consider putting a FIP in place is that it can help transfer value from the older to younger generation.

The gifts of limited partner interests to the children should be free of UK inheritance tax provided the donor survives for seven years after making them. Provided care is taken with the structure, the value gifted should then be outside of the scope of inheritance tax on the donor’s death.

If the donor is a US person, they must also consider US gift tax, but this is often covered by their lifetime exempt allowance (ex US citizens need to be very careful of the covered expatriate rules).

Provided the FIP is funded with cash, there should be no capital gains tax on establishment.

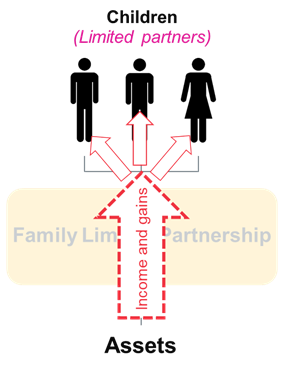

On an ongoing basis the FIP will generally be considered transparent for tax purposes, meaning that each limited partner will be taxed on their “share” of the income and gains realised on the underlying assets:

In practice the general partnership interest is sometimes held via a corporate (for limited liability) and it can be helpful from a US perspective for one parent to fund the FIP whilst the other holds the general partnership interest (whether directly or indirectly).

The limited partners can make use of their respective personal allowances, reliefs and marginal tax rates when calculating their liability (which can be very beneficial if they pay tax at materially lower rates than the older generation). For limited partners with tax exposure in both the UK and the US it should be possible to claim treaty relief and credit one liability against the other, thereby avoiding double taxation.

The FIP documentation can place restrictions on how partnership interests can be dealt with (e.g. limiting the ability of the children to use them as security for debts, or to transfer their interests to others). It will also usually give the general partner(s) (i.e. the older generation) control over the day to day running of the FIP (such as how its funds are invested) and how value can be extracted.

Whilst the children are young, the older generation will often use this control to retain most of the profits in the FIP, only distributing what is necessary for the limited partners to settle their personal tax liabilities.

Over time, the children can be allowed more access and input as they become more mature. It may be appropriate to transfer the general partnership interests to them in due course, or simply wind up the FIP entirely once it has served its purpose.

We have referred elsewhere to the fact that FIPs are generally tax transparent. Whilst this is often seen as an attraction, it also has several practical implications which need to be taken into account. For example:

Like other forms of wealth structuring, there are also ongoing compliance and administrative obligations for the partnership itself.

Explore our full private wealth offering and expertise using the link below.

Learn more

![]() Thought leadership

Thought leadership

29 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-29-15-31-18-835-6a6a1cc67b233ab23d62a576.jpg)

![]() Thought leadership

Thought leadership

27 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-14-17-26-18-947-6a56713a0b21ee7f9d8cc22f.jpg)

![]() Thought leadership

Thought leadership

20 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-20-16-45-25-984-6a5e50a53778c07e459eb63a.jpg)

![]() Thought leadership

Thought leadership

2 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-01-14-49-03-555-6a4528df2871f60bca6453f5.jpg)

![]() Legal updates

Legal updates

1 July 2026

Want more Burges Salmon content? Add us as a preferred source on Google to your favourites list for content and news you can trust.

Update your preferred sourcesBe sure to follow us on LinkedIn and stay up to date with all the latest from Burges Salmon.

Follow us