The UK’s proposals for non-doms and their structures (as of 31 October 2024)

31 Oct 2024

35 min read

This website will offer limited functionality in this browser. We only support the recent versions of major browsers like Chrome, Firefox, Safari, and Edge.

Update 11 March 2025: Please read our updated summary, which and takes into account both changes made to the draft legislation since then and the additional analysis which we have carried out in the meantime. Whilst the proposals remain in draft form at the date of publication, the Finance Bill implementing them has passed the report stage in Parliament and so is likely to be enacted in its current form.

Read the updated versionIn some ways the Autumn Budget confirmed what we already knew or expected. The UK’s tax regime for non-domiciled individuals and their structures will change from 6 April 2025 and be replaced by a new regime based on residence rather than domicile.

However, the technical note issued by the Treasury[1] and the accompanying draft legislation[2] provided much needed clarity and did include a number of surprises as to how the new law will work in practice.

This article summarises where the proposed changes now stand and also flags other announcements from the Budget which could be relevant to those affected by the non-dom reforms.

Please note that the proposals remain in draft form at the date of publication and it is absolutely possible that there could be material changes before the relevant laws are enacted.

The latest version of the proposals will not be as bad as some had feared but nor will they be as favourable as others had hoped. Whatever one’s views of them, they represent a very material change from the status quo and any individuals or trustees with an international connection should be considering how they could be impacted.

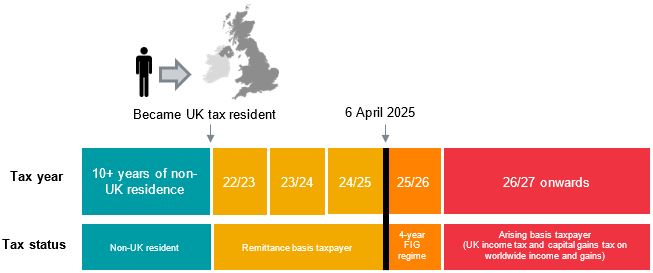

First of all, the remittance basis regime will be replaced with effect from 6 April 2025. Those moving to the UK will be able to claim a new special status in their first four years of UK residence, during which time they will be exempt from UK tax on all foreign income and gains and can bring those funds into the UK without any further income tax or capital gains tax. However, the government appears to have rowed back on previous proposals to extend this four-year regime to UK investment income as well.

There will be two transitional reliefs for individuals, one which will offer a form of rebasing for foreign assets and another which will allow foreign income and gains from previous years to be remitted at a more attractive rate.

The UK’s inheritance tax (“IHT”) rules are also going to change, again with effect from 6 April 2025, such that individuals will be exposed to IHT on their worldwide assets if they have been UK tax resident for 10 or more of the previous 20 tax years (referred to in the technical note as being “Long-Term Resident”).

Once an individual becomes “Long-Term Resident” they will retain that status for as long as they are UK tax resident. They will also remain Long-Term Resident for a number of tax years after they cease to be UK tax resident, with the length of this “tail” ranging from 3 to 10 tax years depending on how long they were UK tax resident prior to leaving.

Trusts established by non-domiciled individuals will also lose many of the UK tax protections which they have enjoyed to date. In particular:

Those affected should take advice and consider their options now so as to determine what steps to take before the end of the tax year.

We have been saying for some time that we thought the non-dom reforms would be implemented with effect from 6 April 2025 and the Autumn Budget confirmed that this is the government’s intention.

Whilst nothing is entirely guaranteed until the legislation is actually passed, clients should be planning on the basis that the changes will come into force at the beginning of the next tax year.

The existing income tax and capital gains tax regime for non-doms (the remittance basis) will be abolished for foreign income and gains arising on or after 6 April 2025.

It will be replaced by a new special status which can be claimed during the first four years of tax residency in the UK. This has been referred to as the “4-year FIG regime” (FIG = Foreign Income and Gains).

Comparing the old and new regimes

| The current remittance basis regime | The new 4-year FIG regime | |

| Criteria | Non-UK domiciled under common law and not deemed domiciled | Non-UK tax resident for at least 10 consecutive years before becoming UK tax resident |

| Maximum length | 15 tax years | 4 tax years |

| Taxation of foreign income and gains (including trust distributions) | Tax free unless remitted, but subject to income tax or capital tax as appropriate if brought into or used in the UK | Tax free, even if brought into or used in the UK |

| Details to provide to HMRC of foreign income and gains | Foreign income and gains are not reported to HMRC unless they are remitted, in which case the amount of remitted income and gains must be reported | Claimants must quantify all foreign income and gains which are being relieved by the new regime and include details in a tax return |

Effect of the new regime

Individuals claiming the status will not pay any UK tax on most forms of foreign income and gains arising in the tax years for which they make the claim.

They can also freely bring such funds into the UK without further tax (albeit that bringing the funds into the UK could expose them to IHT as they would then become UK situated assets).

Prior to the election, Labour hinted at providing some tax relief for UK investment income arising in the four years as well. They said: “We will consider whether there should be an investment incentive during the four-year window, so that UK investment income is free of UK tax and not disincentivised versus investment elsewhere in the world.”[3] There is no mention of this in the latest technical note or draft legislation and so we assume the idea has been dropped.

Someone claiming the 4-year FIG regime can receive distributions from a non-UK resident trust free of UK income tax and capital gains tax. Such distributions will not “match” to income or gains in the trust.

Making a claim will have some drawbacks, such as causing the claimant to lose their income tax Personal Allowance and the capital gains tax Annual Exempt Amount. Foreign losses will also not be allowable as deductions from taxable gains.

Criteria

To be eligible, an individual must not have been UK tax resident in any of the 10 tax years preceding the four-year period.

The 4-year FIG regime will be optional. Individuals will be able to claim the new status in any or all of their first four years of UK tax residence after such a 10-year period of non-residence.

Residence will be tested using the UK’s statutory residence test (explained here: An introduction to Residence and Domicile) for tax years 2013/14 and later and a person’s status under any applicable double tax treaties will be irrelevant. “Split years” will count as full UK tax years. Tax years prior to 2013/14 are tested using the pre-statutory residence test rules.

Those eligible can choose to claim the status in relation to only income, or only gains, rather than both if they wish and will even be able to specify that it applies to some sources of foreign income or gains but not others. This could be beneficial if, for example, the individual would do better by applying a double tax treaty to some income or gains. Any form of claim will cause the loss of the income tax Personal Allowance and capital gains tax Annual Exempt Amount.

For those who meet that criteria and first became tax resident in the UK in the 2022/23, 2023/24 or 2024/25 tax year, such that they will have been UK resident for fewer than 4 tax years as of 6 April 2025, they will be able to claim the 4-year FIG regime for whatever is left of their first 4 years of UK tax residence.

For example:

Comment

Linking access to the new regime to residence rather than domicile will make it simpler to apply and give greater certainty to taxpayers.

It will be available for a much shorter period than the current remittance regime (4 tax years as opposed to a maximum of 15). However, where the new regime does apply, it will be more generous than the existing remittance basis in a number of ways. In particular:

Those who are eligible for the 4-year FIG regime will also be eligible for a modified version of the existing Overseas Workday Relief (OWR) regime.

This will allow UK tax resident employees who perform all or some of their duties outside of the UK to claim tax relief on the remuneration relating to their non-UK duties. The relieved remuneration will be entirely free of UK income tax but the relief will be capped at the lower of (per tax year):

Under the current regime OWR can only be claimed for a maximum of 3 tax years but under the new regime it can be claimed for up to 4 so as to align with the 4-year FIG regime.

The claim for OWR will be separate to any claim for the 4-year FIG regime.

There will be two main transitional rules in relation to the income tax and capital gains aspects of the new regime for individuals:

Rebasing relief

There will be a form of rebasing relief for individuals who have claimed the remittance basis in the past. Where available, this can be used to rebase personally held foreign assets to their market value as of 5 April 2017.

The main criteria are as follows:

The existing rebasing relief for those who became deemed domiciled with effect from 6 April 2017 will also continue to be available.

The Temporary Repatriation Facility

There will be a “Temporary Repatriation Facility” (the “TRF”) available to those who have been subject to the remittance basis in any tax year up to and including 2024/25.

The TRF will be available for three tax years and will allow individuals to remit pre-6 April 2025 foreign income and gains at a flat rate of either 12% or 15% as follows (known as the “TRF Charge”):

| Tax Year | TRF Change |

| 2025/26 | 12% |

| 2026/27 | 12% |

| 2027/28 | 15% |

In order to use the TRF, individuals will need to designate amounts or assets (“designated funds”) and pay the relevant TRF charge in relation to them. There is no need to prove that the designated funds are actually foreign income or gains and there is no obligation to physically remit them. If and when there is a remittance of the designated funds it will be tax-free.

Note that:

In relation to trust distributions, to the extent that these have been made prior to 6 April 2025 and represent FIG, they can be designated and benefit from the TRF. Capital distributions made from Trusts within the three years that the TRF will be available can also benefit to the extent that they match to income and gains which arose within the trust prior to 6 April 2025.

Remittances are commonly made from “mixed funds” (i.e. accounts or assets which comprise various elements of foreign income and gains and capital). There are complex ordering rules for determining which elements of a mixed fund are extracted in what order but these will be changed so that designated funds will be deemed to be remitted first.

For example, if an individual has a non-UK bank account containing £100,000 and they designate £25,000 of that in 2025/26, they will pay the TRF Charge on the designated funds (12% of £25,000 = £3,000). If they then remit £25,000 from the account they will be deemed to have remitted the designated £25,000 first and will pay no further tax. In other words, designated funds are deemed to rise to the top of any mixed fund.

It will also be possible to create a “designated account” in which to pool designated funds from other sources.

A person’s exposure to IHT is currently tested by reference to domicile. From 6 April 2025 the UK will move to a residence-based system instead.

The technical note published by the Treasury uses the term “Long-Term Resident” to describe someone who satisfies the new residence-based test.

Comparing the old and new regimes

For the purposes of this article “non-UK assets” includes both non-UK situated assets and some UK situated assets which benefit from special IHT treatment (such as holdings in authorised unit trusts) whilst “UK assets” includes those deriving their value from UK residential property (to the extent of such derivation). The status of some other assets (such as UK gilts) is already tested by reference to residence and will not change.

| The current, domicile based, regime | |

| Status | IHT exposure |

| UK domiciled or deemed domiciled | IHT on UK assets and non-UK assets |

| Otherwise | IHT on UK assets only |

| The new , residency based, regime | |

| Status | IHT exposure |

| “Long-Term Resident” | IHT on UK assets and non-UK assets |

| Otherwise | IHT on UK assets only |

The concept of “Long-Term Resident”

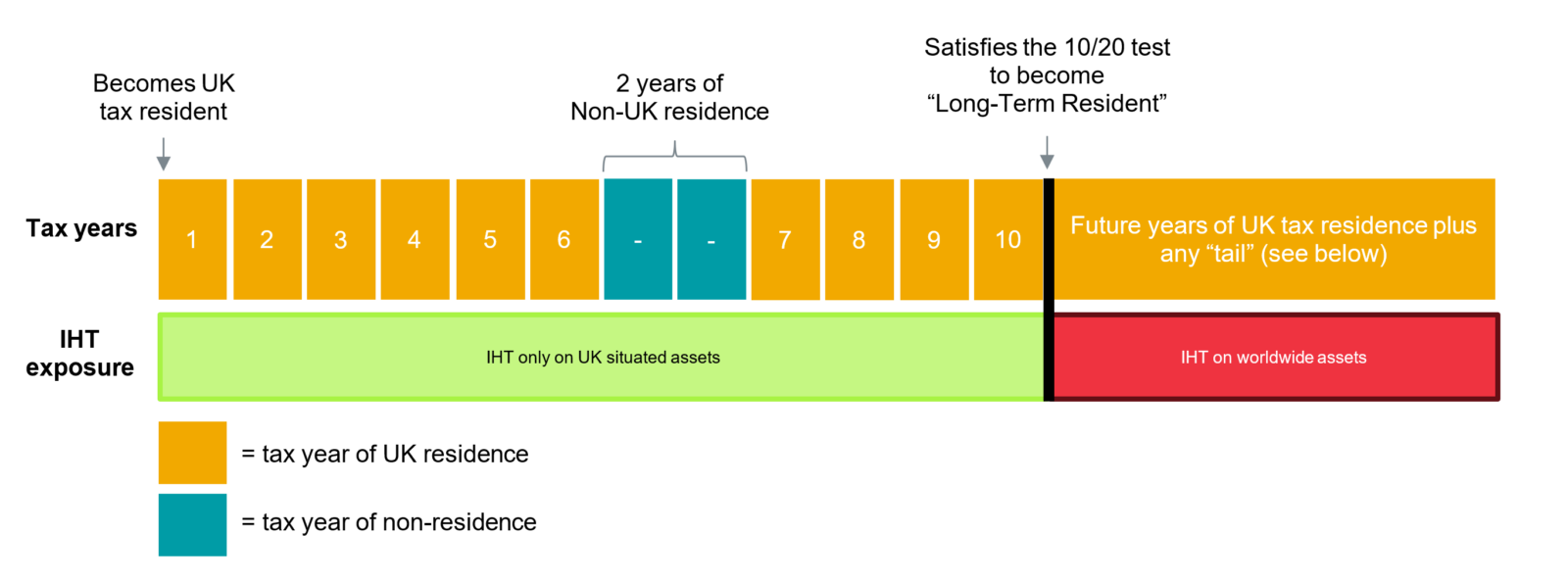

The core of the new test is that a person will be “Long-Term Resident” in a given tax year (and so exposed to IHT on their worldwide assets) if they have been UK tax resident in 10 or more of the preceding 20 tax years.

So, subject to the points made below, the starting point is that a person will be Long-Term Resident with effect from 6 April 2025 if they have been UK tax resident in 10 or more of the tax years between 2005/06 and 2024/25 inclusive.

The most obvious example of this will be at the beginning of the 11th year after 10 consecutive tax years of being UK tax resident. However, it can also apply to those with gaps between years of UK tax residence as shown in the diagram below:

If a person ceases to be UK tax resident after 9/20 tax years, then they will never become Long-Term Resident.

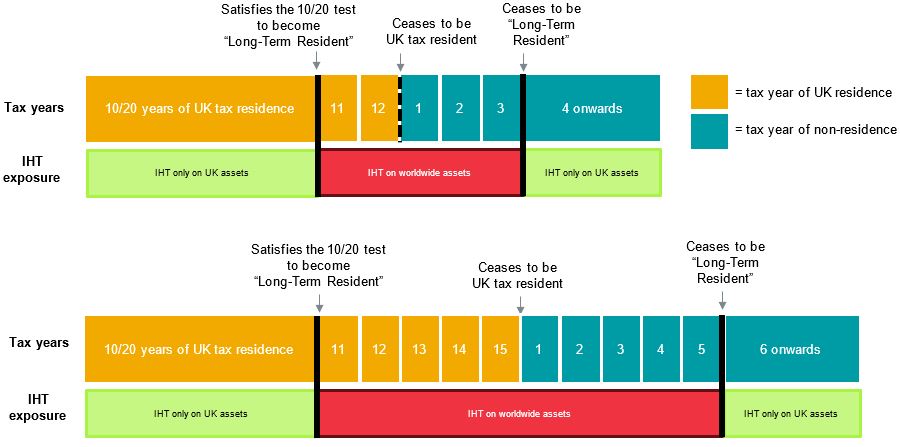

However, once a person satisfies the 10/20 test and becomes Long-Term Resident, they will retain that status for as long as they remain UK tax resident and for a number of years even after ceasing to be UK tax resident.

The number of years of non-UK residence required to lose Long-Term Resident status can be thought of as a “tail”. The default length of the tail is 10 tax years but it can be shortened if the individual was not UK tax resident in all 20 of the tax years prior to their departure:

| No. of years of UK tax residence in the 20 prior to departure | Length of the “tail” |

| Tax resident in 9 or fewer of the 20 years | Never Long-Term Resident and no tail |

| Tax resident in 10 – 13 of the 20 years | 3 tax years |

| Tax resident in 14 – 19 of the 20 years | Add one year (to the 3 year starting point) for each additional year of tax residence above 13. So: 14 years of tax residence = a 4 year tail 17 years of tax residence = a 7 year tail and so on |

| Tax resident in all 20 years | 10 tax years |

Two visual examples of how the tail will operate in practice are shown below:

A different rule for those aged 20 and under

The government clearly realised that if the 10/20 test applied to everyone then many children who have only ever lived in the UK would not satisfy it. E.g. a 9 year old would not yet have accrued 10 years of UK tax residence.

To address this issue, those aged 20 or younger will be Long-Term Resident if they have been UK resident for at least 50% of the tax years since their birth.

That would suggest that a child under the age of 1 will not be Long-Term Resident in the tax year of their birth even if born in the UK.

Transitional rules for some non-doms

When the IHT changes were first announced there was a concern that individuals who had ceased to be exposed to IHT on their worldwide estates under the domicile based tests would be pulled back into the IHT net by the new regime.

There is a transitional rule for those who would otherwise be in this position. The practical impact is that those who:

will either not become Long-Term Resident at all or will have a maximum “tail” of three tax years.

Most such individuals will fall into one of three categories:

| Category | First tax year of non-UK residence (“Year X”) | No. of years of UK residence in the 20 tax years preceding Year X | IHT status and “tail” |

| “Past leavers” | 2022/23 or earlier | N/A | Never become Long-Term Resident so no “tail” |

| “Recent leavers but short stayers“ | 2023/24 – 2025/26 | 14 or fewer | Never become Long-Term Resident so no “tail” |

| “Recent leavers but long stayers” | 2023/24 – 2025/26 | 15 or more | Become Long-Term Resident on 6 April 2025 but lose that status at the beginning of their 4th tax year of non-UK residence E.g., if 2025/26 is the first year of non-UK residence then the individual will lose Long-Term Resident status on 6 April 2028. |

The impact on gifting

From 6 April 2025, whether a gift of a non-UK asset is potentially within the scope of the seven year rule for IHT (such that there could be an IHT charge if the donor dies within seven years of making it) will depend on whether donor is Long-Term Resident at the time they make the gift.

In other words:

The spouse exemption

The full spouse exemption (i.e. 100% relief from IHT) will be available between spouses who are both Long-Term Resident.

If a gift (on lifetime or death) is made from a spouse who is Long-Term Resident to one who is not then the spouse exemption will be capped unless the recipient spouse elects to be treated as a Long-Term Resident.

If the recipient spouse makes such an election then they will be treated as Long-Term Resident until they have been non-UK resident for 10 consecutive tax years.

There are also transitional rules for elections which have already been made under the current regime and elections which span the two regimes.

Double tax treaties

The UK has a limited number of double tax treaties which relate to IHT. The technical note confirms that the new rules will not impact the operation of these which is particularly good news for individuals who currently enjoy beneficial tax treatment under them (such as clients who are UK resident but domiciled in India).

The tax treatment of trusts established by non-domiciled settlors will change considerably.

The current position

Currently, certain trusts established by individuals who are neither domiciled nor deemed domiciled at the relevant time benefit from “protected trust” status. This generally means that gains and foreign income arising within the trust are not taxable on the settlor(s) and are only subject to UK tax when distributions are made to UK resident beneficiaries.

The changes

From 6 April 2025 the protected trust regime will effectively cease to apply, meaning that income and gains in affected trust structures could become taxable on any UK resident settlor(s) from that date.

In practice, this appears unlikely to impact trusts which:

(a) have no living settlors; or

(b) have only non-UK resident settlors (assuming the settlor(s) are not planning on moving to the UK); or

(c) have only settlors who claim the benefit of the 4-year FIG regime (these trusts will be impacted if and when the settlor stops claiming that regime).

For trusts with UK resident settlors who cannot (or do not) claim the 4-year FIG regime, the implications will depend upon a number of factors, including the terms of the trust (exclusions could be particularly significant in determining which forms of income or gain can be attributed to the settlor) and the nature of the trust’s investments.

Although the loss of protected trust status will be a blow, there are some changes to the way in which income and gains will be attributed from trusts to settlors which will soften it slightly. For example:

The “EU defence” against income attribution from trusts is being removed but in our experience this was rarely used in practice.

The way in which beneficiaries of non-UK resident trusts are taxed will not change in principle. However:

Comment

Existing structures should be reviewed now to determine:

The current position

At a high level, trusts established by non-domiciled individuals can benefit from a broad exemption from IHT for so long as they only hold assets situated outside of the UK. These are known as “excluded property trusts”.

UK situated assets held at trust level (and non-UK situated assets which derive their value from UK residential property) are already within the scope of IHT even when held in such trusts.

The changes

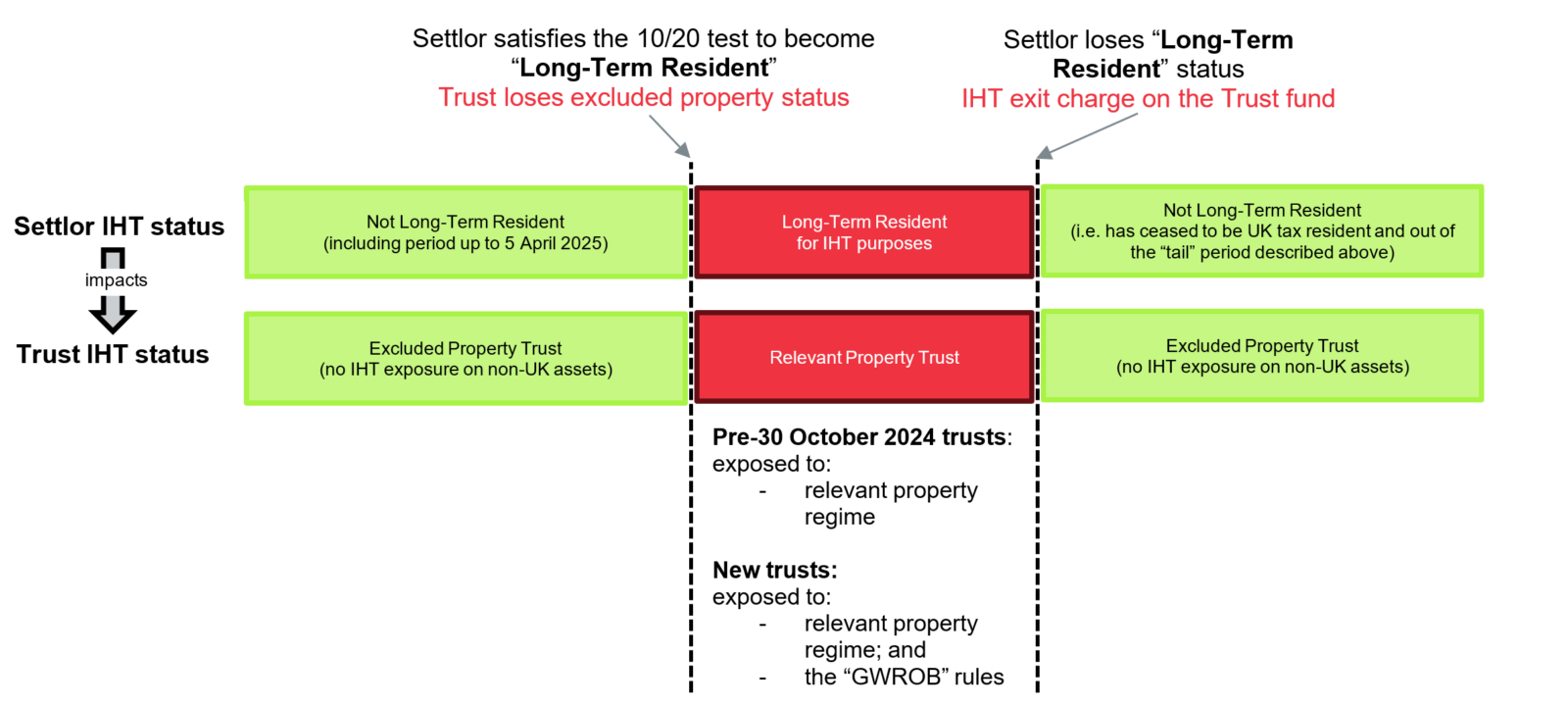

From 6 April 2025 the IHT exposure of a trust will no longer be determined by the domicile status of its settlor when it was established or funded.

Instead, assets held in a trust will only be excluded property (i.e. not subject to IHT charges) if:

In other words, the IHT status of a trust will now vary depending on the status of the settlor and a trust may move in and out of the IHT net as the settlor acquires or loses Long-Term Resident status. By way of example, this can be visualised as follows:

There is no full grandfathering for existing trusts, there are important differences in the IHT treatment of trusts established and funded prior to 30 October 2024 as compared to those established or funded on or after the date of the Budget:

The impact for trusts already in existence as of 30 October 2024

As and when the settlor of such a trust becomes Long-Term Resident, the trust fund will be exposed to the UK’s “relevant property regime”.

In practice this could mean IHT charges at a rate of up to 6%:

That last point is potentially a nasty surprise for trusts and an important matter to bear in mind if a Long-Term Resident settlor may leave the UK. Double tax treaties with some countries (including, for example, the US) can mitigate the issue in some scenarios but the point will need careful analysis.

However, such pre-existing trusts do retain some IHT advantages in that the trust fund will not be caught by the gift with reservation of benefit (“GWROB”) rules which can deem trust assets to be part of the estate of the settlor for IHT purposes in addition to being caught by the relevant property regime. This avoids potential double taxation.

The impact for trusts established or funded on or after 30 October 2024

The status of new trusts will also be determined by whether or not the settlor is a Long-Term Resident. However, as and when the settlor has that status the trust will potentially face two forms of IHT exposure:

Again, if a settlor ceases to be Long-Term Resident, such that the trust becomes an excluded property trust, there will be an IHT exit charge.

To the extent that pre-existing trusts receive additional funding on or after 30 October 2024, such additional funds will be subject to this new regime.

Trusts with UK domiciled but non-UK resident settlors

Trusts established by UK domiciled settlors are currently within the relevant property regime. This is the case even if the settlor is non-UK resident.

That will change under the new rules. For example, if a settlor is UK domiciled but is not Long-Term Resident on 6 April 2025 then the trust will become an excluded property trust (such that non-UK assets in the trust will be outside of the scope of IHT) from that date.

In many cases this will be welcomed. However, the change in status will trigger an exit charge of up to 6% of the value of the trust fund at the time and so thought should be given as to how to fund this if it is likely to be relevant.

Trusts with deceased settlors

If the settlor of a trust has died then the IHT status of non-UK assets in the trust will depend on when the death occurred:

Qualifying Interest In Possession Trusts (a sub-category of life-interest trusts)

Qualifying Interest In Possession Trusts (known as “QIIPs”) are a type of life interest trust. The person who holds the life interest (i.e. who is entitled to the income of the trust) is known as the “life tenant”.

The trust fund of a QIIP is treated for IHT purposes as being owned by the life tenant and is not within the scope of the relevant property regime.

From 6 April 2025 non-UK assets in QIIPs which already existed as of 29 October 2024 will continue to be excluded property (and so outside of the scope of IHT) to the extent they were excluded property on 29 October.

However, in all other cases, non-UK assets in QIIPs will only be excluded property at times when neither the settlor nor the life tenant are Long-Term Resident.

Whilst the Chancellor stated that domicile will cease to be a relevant factor for (most of) UK tax law, it is important to recognise that it will continue to play a role in other aspects of UK law.

For example, a person’s domicile is key to determining which country’s (or countries’) succession laws will apply to their estate on their death and can also impact matters such as divorce proceedings.

Even in the context of taxation, domicile and deemed domicile will continue to important for the application of certain double tax treaties (including, for instance, the UK/US and the UK/India inheritance tax treaties).

Domicile will therefore continue to play a role in UK law for many years to come even after the changes described in this article are implemented.

There were plenty of other announcements in the Budget which could impact those affected by the non-dom changes. These include:

We have a vast amount of experience advising non-domiciled individuals and their structures, as well as those moving to and from the UK.

We can advise you as to how the new regime might impact you, help you plan your affairs accordingly and assist you in making the most of the transitional rules.

[1] Reforming_the_taxation_of_non-UK_individuals.pdf

[2] Draft Finance Bill Measures

[3] Labour’s plan to close the non-dom loopholes

![]() Thought leadership

Thought leadership

20 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-20-16-45-25-984-6a5e50a53778c07e459eb63a.jpg)

![]() Thought leadership

Thought leadership

2 July 2026

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-07-01-14-49-03-555-6a4528df2871f60bca6453f5.jpg)

![]() Legal updates

Legal updates

1 July 2026

![]() Legal updates

Legal updates

9 June 2026

![]() Legal updates

Legal updates

2 June 2026 • 8 min read

/Passle/5d9604688cb6230bac62c2d0/SearchServiceImages/2026-05-12-11-03-07-025-6a0308ebab2914b0981e857f.jpg)

Want more Burges Salmon content? Add us as a preferred source on Google to your favourites list for content and news you can trust.

Update your preferred sourcesBe sure to follow us on LinkedIn and stay up to date with all the latest from Burges Salmon.

Follow us